Transportation Management Systems

Why Most Small Fleet Owners Leave $265,000 on The table every year

The purchasing power advantages that large carriers hold are real. Most of them are also available to a 15-truck fleet. The decision not to claim them costs an estimated $272,000/year.

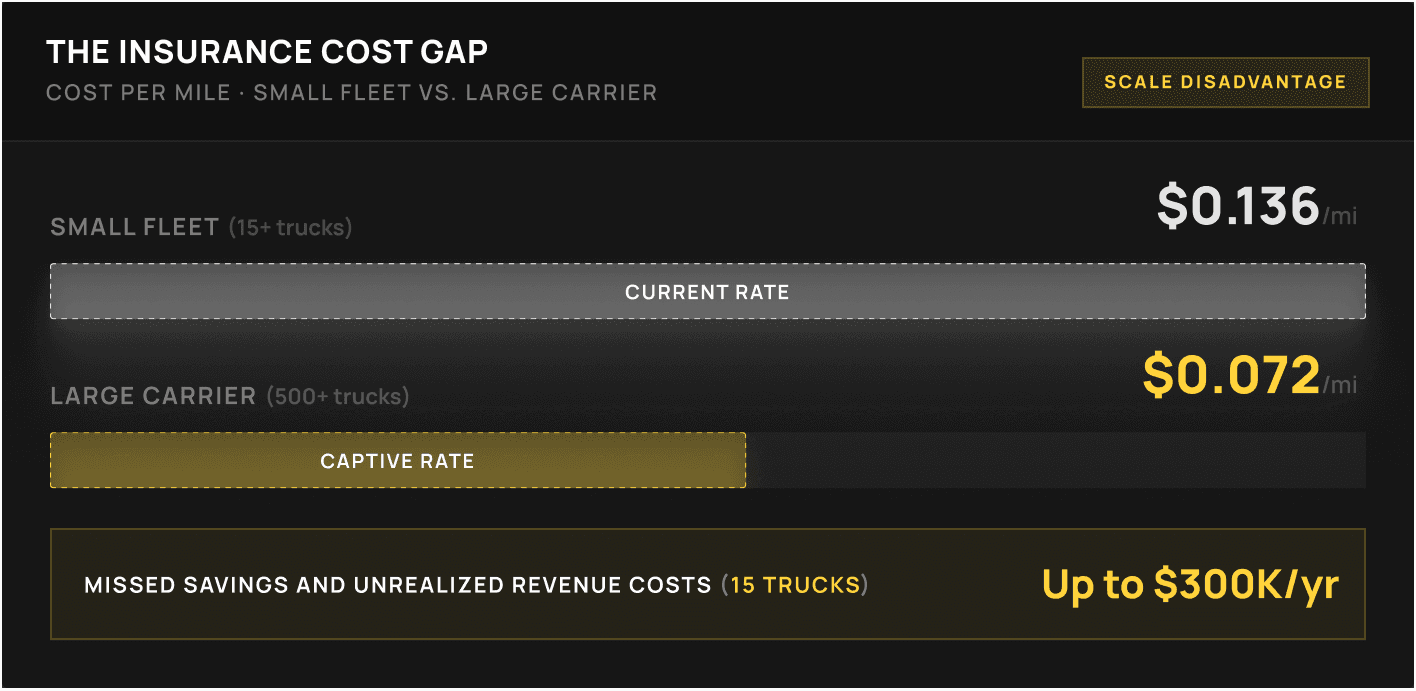

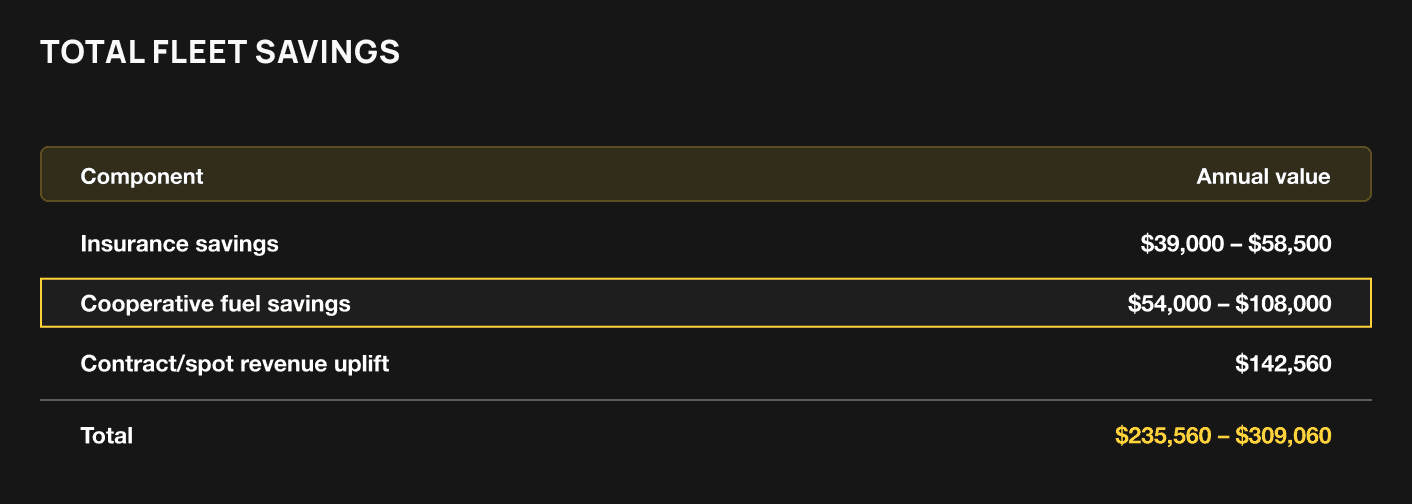

The conventional wisdom in small fleet trucking goes something like this: large carriers have structural advantages that small operators simply cannot access until they grow large enough to qualify for them. It is a reasonable-sounding argument. However, it is largely wrong — and accepting it costs a 15-truck fleet an estimated $235,560 to $309,060 per year in missed savings and unrealized revenue.

According to ATRI's Operational Costs of Trucking research, a 15-truck fleet paid $0.136 per mile for insurance in 2022 compared to $0.072 per mile for a 500-truck fleet. ATRI's 2025 report confirms the gap has only widened since, with industry-wide premiums reaching a record $0.102 per mile in 2024. Equipment financing terms are better for large fleets. Fuel discounts are deeper. Contract freight access is wider. But the majority of these advantages are not locked behind fleet size. They are locked behind organizational decisions that most small fleet owners have not made.

Captive Insurance Is a Goal, Not a Wall

Group captive insurance programs generally require approximately 25 or more power units, five years in business, loss ratios below 35%, and $250,000 or more in annual premiums. Most small fleet owners cite these thresholds as reasons captive insurance is unavailable to them. The more accurate framing is that captive insurance is a strategic goal with a clear roadmap.

Every dollar invested in dashcams, driver training, and preventive maintenance today is a dollar reducing your loss ratio. A fleet building a clean CSA score and a documented safety record is not just running better — it is shortening the distance to captive eligibility. The qualification threshold is not a barrier. It is a finish line with a measurable path behind it.

The counterargument is that group captives require five-year commitments and capital participation that small fleets cannot sustain. This is a legitimate concern for operators with thin cash reserves. The response is practical: higher deductibles combined with a funded claims reserve can deliver 15% to 25% premium savings without captive enrollment. Dashcam discounts add another 5%. For a 15-truck fleet paying approximately $195,000 annually in premiums, those two steps alone recover $39,000 to $58,500 per year without a captive. When captive eligibility arrives, it layers dividend returns on unused premiums and long-term rate stabilization on top of the savings the fleet is already capturing.

The Fuel Discount That Pays for Itself

NASTC's cooperative fuel program has 13,000 member companies. Their collective volume generates per-gallon discounts of $0.25 to $0.50 compared to retail. On a 15-truck fleet burning 18,000 gallons per month, that is $54,000 to $108,000 in annual savings. The membership fee is approximately $2,500 to $3,500 per year. The ROI is not marginal. It is overwhelming — and yet the majority of small fleet owners are not enrolled in a cooperative fuel program.

The excuse is usually that fuel card administration is complex or that the savings are smaller in practice than advertised. The complexity argument does not hold: modern fuel card programs integrate with TMS and accounting software, eliminating manual receipt tracking and IFTA calculation work that already costs small fleet operations 10 to 20 hours per month. And even if the actual per-gallon savings land at the low end — $0.25 per gallon — the annual savings on a 15-truck fleet still exceed $54,000.

The Revenue Gap Is Where Most Operators Lose

The most underestimated purchasing power advantage of scale is not on the cost side. It is on the revenue side. Shippers award annual contracts to carriers who can reliably cover committed lane volumes. A 15-truck fleet can make that commitment. A single-truck operator cannot. The rate premium on contract freight versus current spot market runs 15% to 25%.

At $22,000 per truck per month in gross revenue, moving from a 50/50 contract-to-spot mix to a 70/30 split — while contract rates run 20% above spot — adds approximately $792 per truck per month in revenue without adding a mile or a gallon of diesel. Across 15 trucks, that is $11,880 per month, or $142,560 per year.

The conventional wisdom in small fleet trucking goes something like this: large carriers have structural advantages that small operators simply cannot access until they grow large enough to qualify for them. It is a reasonable-sounding argument. However, it is largely wrong — and accepting it costs a 15-truck fleet an estimated $235,560 to $309,060 per year in missed savings and unrealized revenue.

According to ATRI's Operational Costs of Trucking research, a 15-truck fleet paid $0.136 per mile for insurance in 2022 compared to $0.072 per mile for a 500-truck fleet. ATRI's 2025 report confirms the gap has only widened since, with industry-wide premiums reaching a record $0.102 per mile in 2024. Equipment financing terms are better for large fleets. Fuel discounts are deeper. Contract freight access is wider. But the majority of these advantages are not locked behind fleet size. They are locked behind organizational decisions that most small fleet owners have not made.

Captive Insurance Is a Goal, Not a Wall

Group captive insurance programs generally require approximately 25 or more power units, five years in business, loss ratios below 35%, and $250,000 or more in annual premiums. Most small fleet owners cite these thresholds as reasons captive insurance is unavailable to them. The more accurate framing is that captive insurance is a strategic goal with a clear roadmap.

Every dollar invested in dashcams, driver training, and preventive maintenance today is a dollar reducing your loss ratio. A fleet building a clean CSA score and a documented safety record is not just running better — it is shortening the distance to captive eligibility. The qualification threshold is not a barrier. It is a finish line with a measurable path behind it.

The counterargument is that group captives require five-year commitments and capital participation that small fleets cannot sustain. This is a legitimate concern for operators with thin cash reserves. The response is practical: higher deductibles combined with a funded claims reserve can deliver 15% to 25% premium savings without captive enrollment. Dashcam discounts add another 5%. For a 15-truck fleet paying approximately $195,000 annually in premiums, those two steps alone recover $39,000 to $58,500 per year without a captive. When captive eligibility arrives, it layers dividend returns on unused premiums and long-term rate stabilization on top of the savings the fleet is already capturing.

The Fuel Discount That Pays for Itself

NASTC's cooperative fuel program has 13,000 member companies. Their collective volume generates per-gallon discounts of $0.25 to $0.50 compared to retail. On a 15-truck fleet burning 18,000 gallons per month, that is $54,000 to $108,000 in annual savings. The membership fee is approximately $2,500 to $3,500 per year. The ROI is not marginal. It is overwhelming — and yet the majority of small fleet owners are not enrolled in a cooperative fuel program.

The excuse is usually that fuel card administration is complex or that the savings are smaller in practice than advertised. The complexity argument does not hold: modern fuel card programs integrate with TMS and accounting software, eliminating manual receipt tracking and IFTA calculation work that already costs small fleet operations 10 to 20 hours per month. And even if the actual per-gallon savings land at the low end — $0.25 per gallon — the annual savings on a 15-truck fleet still exceed $54,000.

The Revenue Gap Is Where Most Operators Lose

The most underestimated purchasing power advantage of scale is not on the cost side. It is on the revenue side. Shippers award annual contracts to carriers who can reliably cover committed lane volumes. A 15-truck fleet can make that commitment. A single-truck operator cannot. The rate premium on contract freight versus current spot market runs 15% to 25%.

At $22,000 per truck per month in gross revenue, moving from a 50/50 contract-to-spot mix to a 70/30 split — while contract rates run 20% above spot — adds approximately $792 per truck per month in revenue without adding a mile or a gallon of diesel. Across 15 trucks, that is $11,880 per month, or $142,560 per year.

The conventional wisdom in small fleet trucking goes something like this: large carriers have structural advantages that small operators simply cannot access until they grow large enough to qualify for them. It is a reasonable-sounding argument. However, it is largely wrong — and accepting it costs a 15-truck fleet an estimated $235,560 to $309,060 per year in missed savings and unrealized revenue.

According to ATRI's Operational Costs of Trucking research, a 15-truck fleet paid $0.136 per mile for insurance in 2022 compared to $0.072 per mile for a 500-truck fleet. ATRI's 2025 report confirms the gap has only widened since, with industry-wide premiums reaching a record $0.102 per mile in 2024. Equipment financing terms are better for large fleets. Fuel discounts are deeper. Contract freight access is wider. But the majority of these advantages are not locked behind fleet size. They are locked behind organizational decisions that most small fleet owners have not made.

Captive Insurance Is a Goal, Not a Wall

Group captive insurance programs generally require approximately 25 or more power units, five years in business, loss ratios below 35%, and $250,000 or more in annual premiums. Most small fleet owners cite these thresholds as reasons captive insurance is unavailable to them. The more accurate framing is that captive insurance is a strategic goal with a clear roadmap.

Every dollar invested in dashcams, driver training, and preventive maintenance today is a dollar reducing your loss ratio. A fleet building a clean CSA score and a documented safety record is not just running better — it is shortening the distance to captive eligibility. The qualification threshold is not a barrier. It is a finish line with a measurable path behind it.

The counterargument is that group captives require five-year commitments and capital participation that small fleets cannot sustain. This is a legitimate concern for operators with thin cash reserves. The response is practical: higher deductibles combined with a funded claims reserve can deliver 15% to 25% premium savings without captive enrollment. Dashcam discounts add another 5%. For a 15-truck fleet paying approximately $195,000 annually in premiums, those two steps alone recover $39,000 to $58,500 per year without a captive. When captive eligibility arrives, it layers dividend returns on unused premiums and long-term rate stabilization on top of the savings the fleet is already capturing.

The Fuel Discount That Pays for Itself

NASTC's cooperative fuel program has 13,000 member companies. Their collective volume generates per-gallon discounts of $0.25 to $0.50 compared to retail. On a 15-truck fleet burning 18,000 gallons per month, that is $54,000 to $108,000 in annual savings. The membership fee is approximately $2,500 to $3,500 per year. The ROI is not marginal. It is overwhelming — and yet the majority of small fleet owners are not enrolled in a cooperative fuel program.

The excuse is usually that fuel card administration is complex or that the savings are smaller in practice than advertised. The complexity argument does not hold: modern fuel card programs integrate with TMS and accounting software, eliminating manual receipt tracking and IFTA calculation work that already costs small fleet operations 10 to 20 hours per month. And even if the actual per-gallon savings land at the low end — $0.25 per gallon — the annual savings on a 15-truck fleet still exceed $54,000.

The Revenue Gap Is Where Most Operators Lose

The most underestimated purchasing power advantage of scale is not on the cost side. It is on the revenue side. Shippers award annual contracts to carriers who can reliably cover committed lane volumes. A 15-truck fleet can make that commitment. A single-truck operator cannot. The rate premium on contract freight versus current spot market runs 15% to 25%.

At $22,000 per truck per month in gross revenue, moving from a 50/50 contract-to-spot mix to a 70/30 split — while contract rates run 20% above spot — adds approximately $792 per truck per month in revenue without adding a mile or a gallon of diesel. Across 15 trucks, that is $11,880 per month, or $142,560 per year.

Transform your freight operations and leap ahead of the competition.

© Hemut co All Rights Reserved 2026

Transform your freight operations and leap ahead of the competition.

© Hemut co All Rights Reserved 2026

Transform your freight operations and leap ahead of the competition.

© Hemut co All Rights Reserved 2026